Sigh of relief from borrowers as RBA makes its marginal call

The Reserve Bank of Australia (RBA) has kept the cash rate on hold at 4.35 per cent despite persistent inflation testing its resolve.

Stubbornly high inflation has not been quite threatening enough to force the RBA’s hand.

The official cash rate was kept on hold at 4.35 per cent at the Reserve Bank’s Tuesday (6 August) meeting but Reserve Bank Governor Michele Bullock has all but ruled out a rate cut this year.

The RBA Board noted that the economic outlook is uncertain and recent data demonstrated that the process of returning inflation to target has been “slow and bumpy”.

While the hold decision had been expected by all four big banks and about 80 per cent of economists, the tone of the announcement suggested a hike could still be imminent.

“Inflation in underlying terms remains too high, and the latest projections show that it will be some time yet before inflation is sustainably in the target range,” The RBA’s minutes noted.

“Data has reinforced the need to remain vigilant to upside risks to inflation and the Board is not ruling anything in or out.

“Policy will need to be sufficiently restrictive until the Board is confident that inflation is moving sustainably towards the target range.”

The quarterly rate of core inflation eased back to 0.8 per cent in the June quarter, in line with the RBA’s May forecast and down from 1.0 per cent in the March quarter, taking much of the pressure off the RBA to lift rates.

A slowdown in job growth, a subtle lift in the unemployment rate and concerns about international economies were also at play in keeping rates on hold.

“Momentum in economic activity has been weak, as evidenced by slow growth in GDP, a rise in the unemployment rate and reports that many businesses are under pressure and there is a risk that household consumption picks up more slowly than expected, resulting in continued subdued output growth and a noticeable deterioration in the labour market.”

The RBA noted that there also remains a high level of uncertainty about the overseas situation.

“The outlook for the Chinese economy has softened and this has been reflected in commodity prices.

“Some central banks have eased policy, although they remain alert to the risk of persistent inflation.

“Globally, financial markets have been volatile of late and the Australian dollar has depreciated (while) geopolitical uncertainties remain elevated, which may have implications for supply chains.”

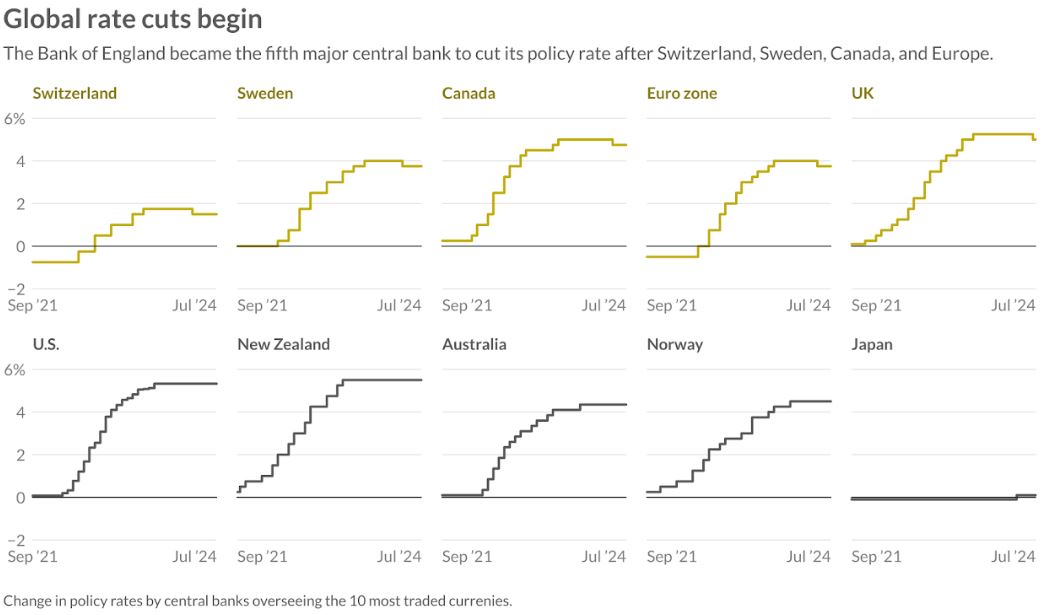

As much of Europe has started to cut rates put in place to tackle global inflation and the US Fed faces increasing pressure to unwind its position the face of economic sluggishness and share market volatility, Australian commentators remain divided on what direction rates might move in this country.

What will the RBA’s next move be?

Graham Cooke, head of consumer research at Finder, said mortgagors were now anxiously waiting for a cash rate cut.

“Millions of Aussie borrowers are experiencing significant mortgage stress due to the fact that their monthly repayments have blown out so much and so rapidly.

“They’re waiting with bated breath for any sign of relief from the RBA.

“The good news is our experts say there’s a 56 per cent chance of a rate cut in the next 12 months; the bad news is 1 in 3 say we will see a rate rise,” Cooke said.

Dr Nalini Prasad of UNSW Sydney, and who has previously worked at the RBA, said the pressure to raise rates would exceed any desire to lower them.

“The latest release of data shows that inflation remains higher than target and I think the RBA will want to increase interest rates to try and bring down inflation rather than risk not doing anything and seeing inflation rise in the future.”

A conflicting view came from Jeffrey Sheen, Professor of Economics, Macquarie University, who said weak economic data would be weighing on the collective minds of the RBA economists.

“Economic growth remains weak, and it will take more time for inflation to finally reach the RBA’s target range.

“There is no need for a change in the cash rate at the moment but by November, I expect the RBA to be ready to cut.”

Associate Professor Evgenia Dechter, School of Economics, UNSW Business School, told API Magazine that there was still the likelihood of a cut this year.

“If the ongoing slowdown in economic activity in Australia persists, it is likely that the RBA’s next move on the cash rate will be a cut rather than an increase.

“If the current trajectory continues, the RBA might lower the cash rate around December or early next year.”

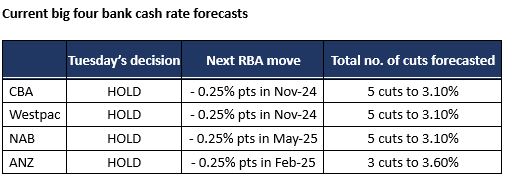

The big four banks all correctly tipped Tuesday’s rate decision and each also expects the RBA to cut rather than raise rates either late this year or into 2025.

Two thirds who weighed in on Finder’s surveying believe mortgage holders are shouldering too much of the burden from the RBA’s attempt to curb inflation.

Shane Oliver, Chief Economist and Head of Investment Strategy, AMP, agreed that mortgage holders were bearing too much of the brunt.

“Tighter fiscal policy in the form of tax hikes and spending cuts or maybe a 1 per cent super levy on everyone would better spread the burden.

“But that would mean politicians would have to do things that are politically unpopular and history shows that they cannot be relied upon to do that.

“So responsibility for controlling inflation should remain with the RBA and that unfortunately means the burden remains on mortgage holders.

“Of course it’s worth recalling that existing mortgage holders were big beneficiaries of falling interest rates in the 1990s, 2000s and 2010s,” Mr Oliver said.

First home buyers’ changing habits

The RBA’s hold decision comes amid pressures on stock markets, increasing concerns about the direction of the global economy and the pricing of potential risks of rising conflict in the Middle East.

Fewer job vacancies and more applicants per job in Australia are increasing concerns that unemployment figures could soon follow.

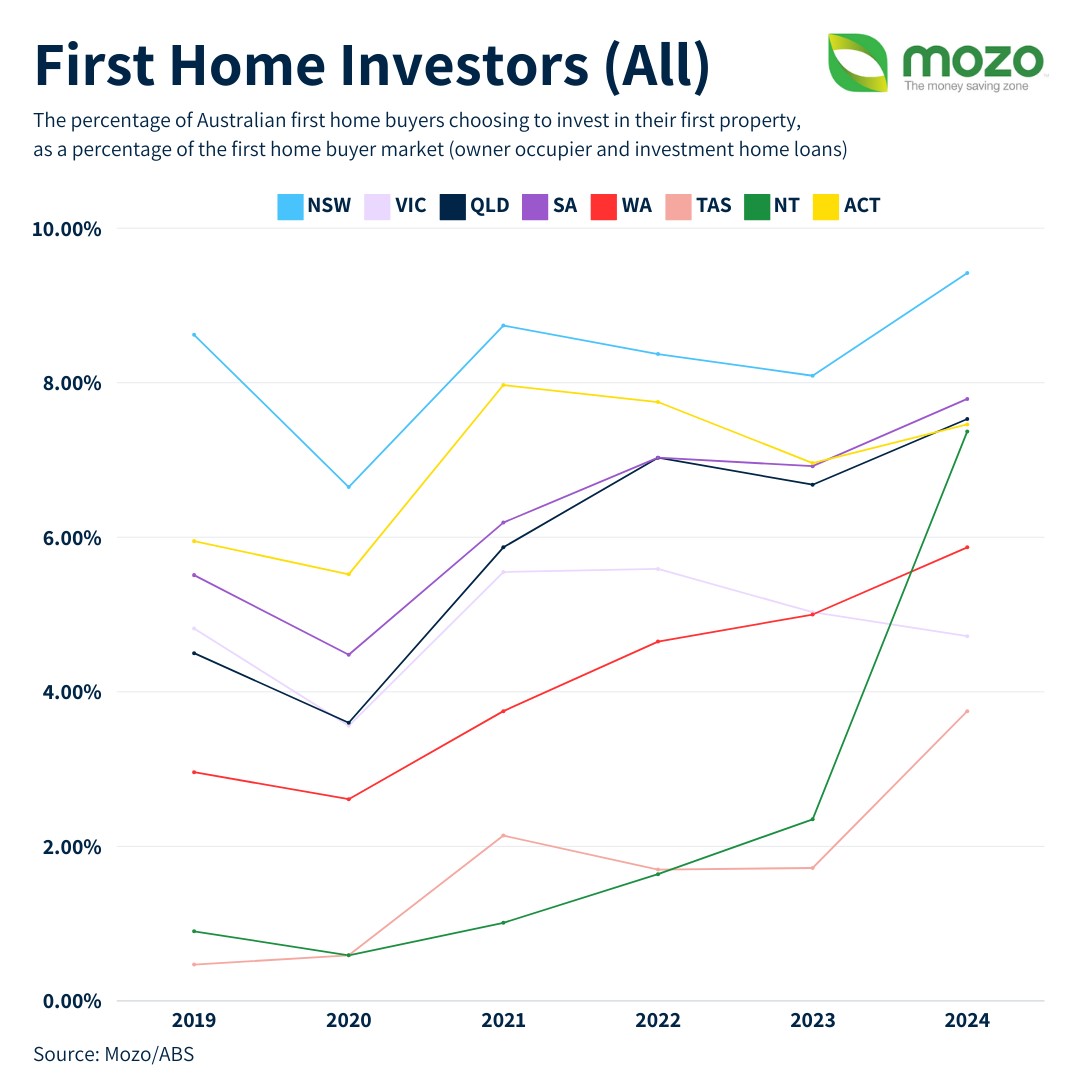

In line with this economic uncertainty, new research from Mozo has revealed a dramatic shift in first home buyer behaviour.

With property prices at record highs and borrowing costs at their highest in a decade, some first home buyers are opting to invest rather than live in the first home they buy.

Mozo analysis of the latest first home buyer lending data reveals the number of first home buyers opting for investment loans has grown by 25 since the Australian Bureau of Statistics (ABS) started publishing the data in July 2019.

Rachel Wastell, Mozo’s personal finance expert, said the RBA’s decision to maintain the cash rate reflects ongoing caution in a volatile economic environment, but it does little to ease the strain on first home buyers.

“While there’s no immediate increase in borrowing costs to new buyers like there are with mortgage holders, the ongoing high rate environment is having a significant impact on purchasing decisions.

“High rates and skyrocketing property prices mean first home buyers are finding homeownership increasingly out of reach, so many are turning to rentvesting as an alternative.”